Gretchen Jacobson Follow @GretchJacob on

Twitter, Meredith Freed, Anthony Damico,

and Tricia Neuman Follow @tricia_neuman on Twitter Published: Jun 06, 2019

Medicare Advantage enrollment has grown

rapidly over the past decade, and Medicare Advantage plans have taken on a larger role in the Medicare

program. This data collection provides current information and trends about Medicare Advantage enrollment, premiums, and

out-of-pocket limits. It also includes analyses of Medicare Advantage plans’

extra benefits and prior authorization requirements.

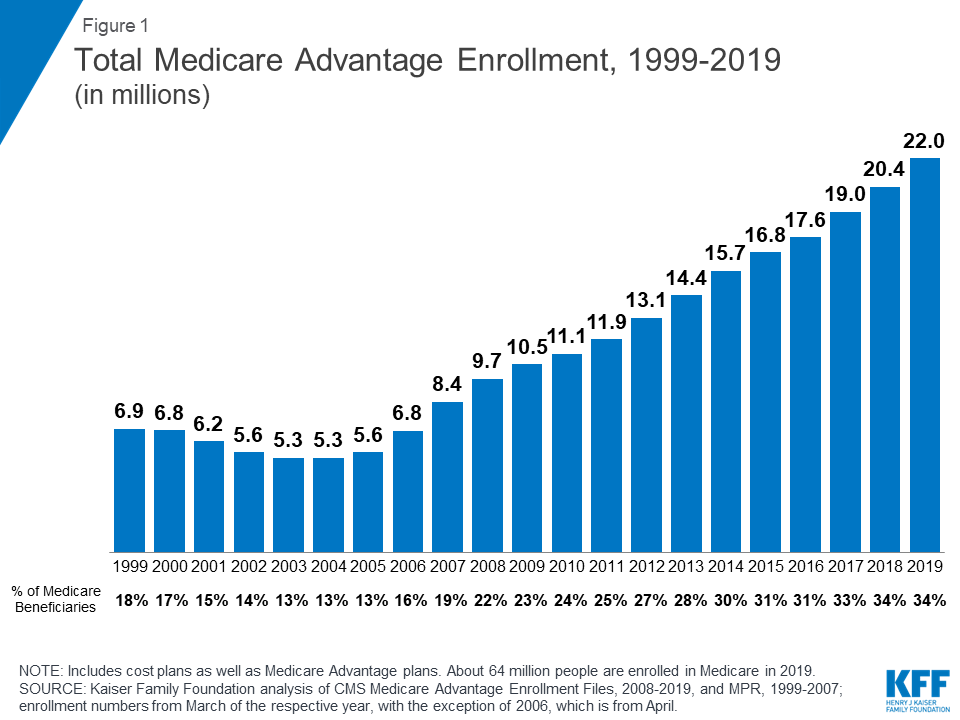

1. Enrollment in

Medicare Advantage has nearly doubled over the past decade

Figure 1: Total

Medicare Advantage Enrollment, 1999-2019 (in millions)

In 2019, one-third (34%) of all Medicare

beneficiaries – 22 million people – are enrolled in Medicare Advantage plans,

similar to the rate in 2017 and 2018. Between 2018 and 2019, total Medicare

Advantage enrollment grew by about 1.6 million beneficiaries, or 8 percent –

nearly the same growth rate as the prior year. The Congressional Budget Office

(CBO) projects that the share of beneficiaries enrolled in Medicare Advantage

plans will rise to about 47 percent by 2029.

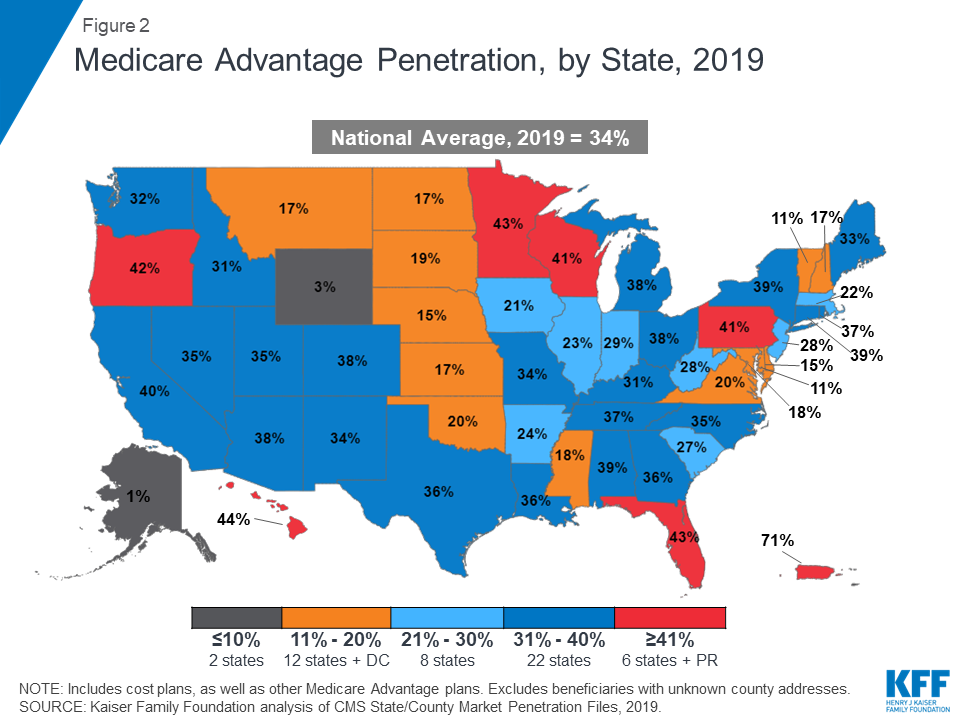

2. The share of

Medicare beneficiaries in Medicare Advantage plans across the United States

ranges from 1% to over 40%

Figure 2: Medicare

Advantage Penetration, by State, 2019

The share of Medicare beneficiaries in

Medicare Advantage plans (including Medicare cost plans), varies across the

country. In 28 states and Puerto Rico, at least 31 percent of Medicare

beneficiaries are enrolled in Medicare Advantage plans, with more than 40

percent of enrollees in six states (HI, FL, MN, OR, WI, PA) and Puerto Rico.

The majority of the Medicare private health plan enrollment in Minnesota has

historically been in cost plans, rather than Medicare Advantage plans, but as

of 2019, most cost plans in Minnesota are no longer offered and have been

replaced with risk-based HMOs and PPOs. Medicare Advantage enrollment is

relatively low (20 percent or lower) in 14 states and the District of Columbia,

including two mostly rural states where it is virtually non-existent (AK and

WY).

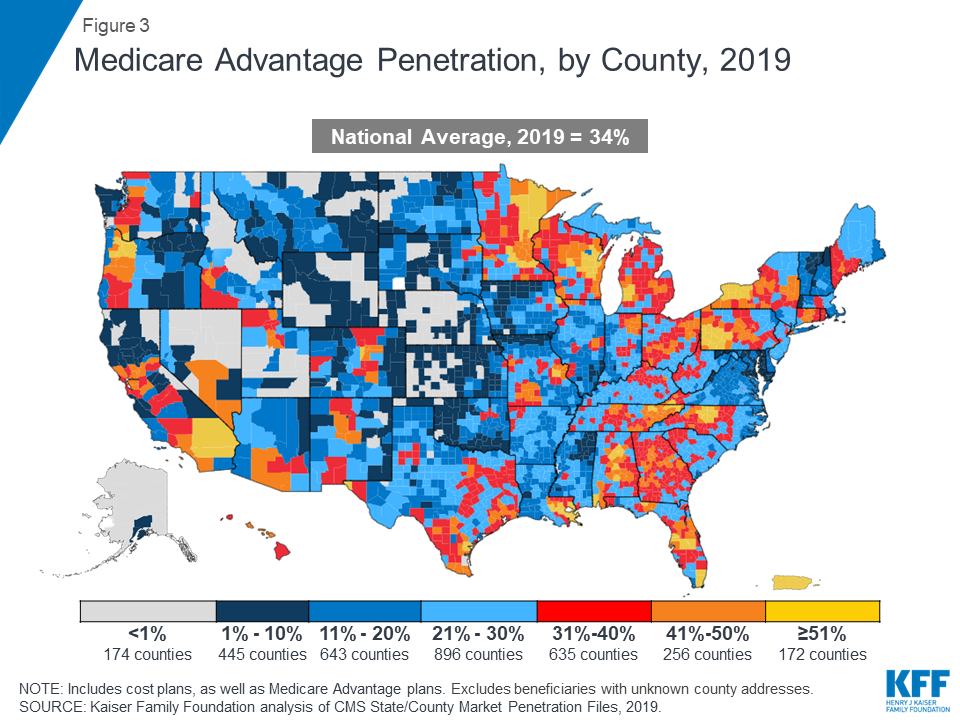

3. The share of

Medicare beneficiaries in Medicare Advantage plans varies across counties from

less than 1% to more than 60%

Figure 3: Medicare

Advantage Penetration, by County, 2019

Within states, Medicare Advantage penetration

varies widely across counties. For example, in Florida, 66 percent of all

beneficiaries living in Miami-Dade County are enrolled in Medicare Advantage

plans whereas only 10 percent of beneficiaries living in Monroe County (Key

West) do so. In 172 counties, accounting for 10 percent of the population, more

than half of all Medicare beneficiaries are enrolled in Medicare Advantage

plans or cost plans. Many of these counties are centered around large, urban

areas, such as Monroe County, NY (66%), which includes Rochester, and Allegheny

County, PA (61%), which includes Pittsburgh. In contrast, in 619 counties,

accounting for 4 percent of Medicare beneficiaries, no more than 10 percent of

beneficiaries are enrolled in Medicare private plans; many of these low

penetration counties are in rural parts of the country but some urban areas,

such as Baltimore City (17%), also have relatively low Medicare Advantage

enrollment.

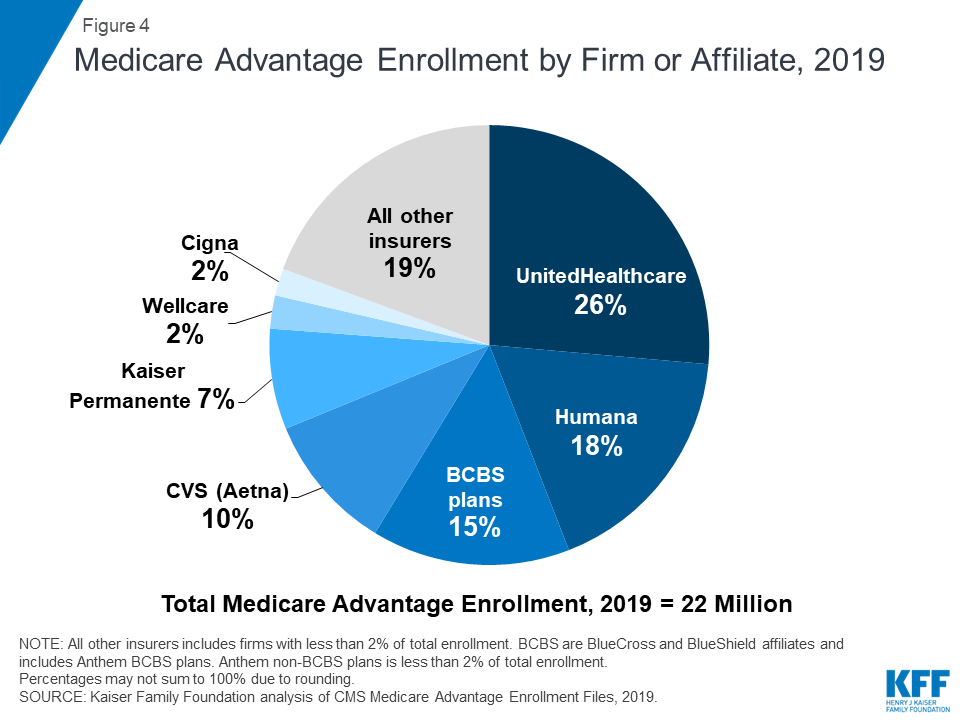

4. Most Medicare

Advantage enrollees are in plans operated by UnitedHealthcare, Humana, or

BlueCross BlueShield (BCBS) affiliates in 2019

Figure 4: Medicare

Advantage Enrollment by Firm or Affiliate, 2019

Medicare Advantage enrollment is highly

concentrated among a small number of firms. UnitedHealthcare and Humana

together account for 44 percent of all Medicare Advantage enrollees nationwide,

and the BCBS affiliates (including Anthem BCBS plans) account for another 15

percent of enrollment in 2019. Another four firms (CVS/Aetna, Kaiser

Permanente, Wellcare, and Cigna) account for another 22 percent of enrollment

in 2019. For the third year in a row, enrollment in UnitedHealthcare’s plans

grew more than any other firm, increasing by about 520,000 beneficiaries

between March 2018 and March 2019. CVS purchased Aetna in 2018 and the combined

company had the second largest growth in Medicare Advantage enrollment in 2019,

increasing by also about 520,000 beneficiaries between March 2018 and March

2019.

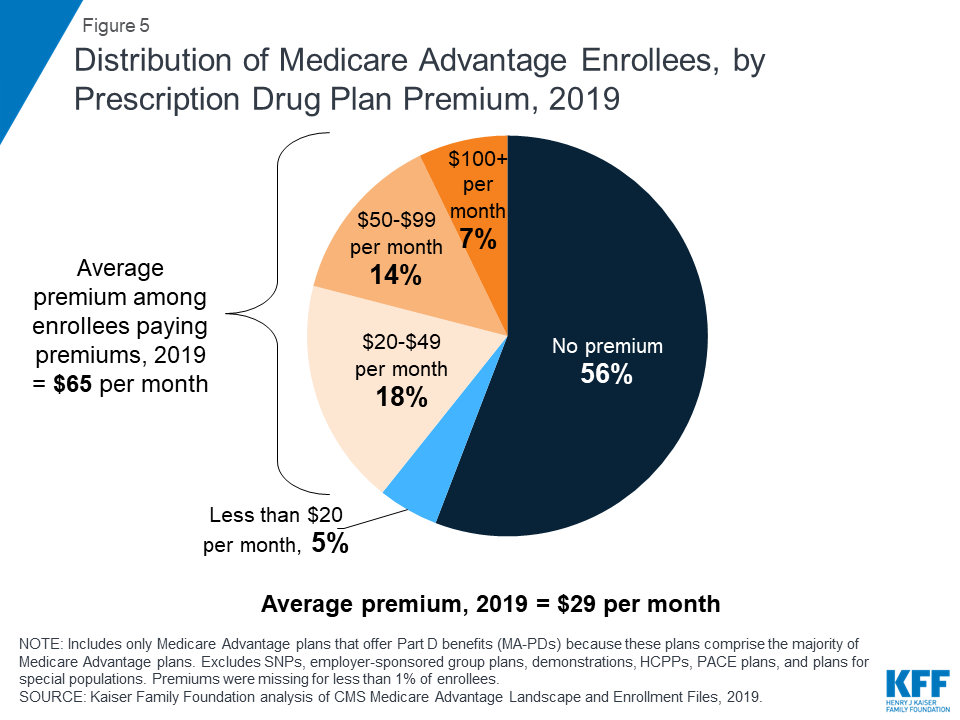

5. Half of Medicare

Advantage enrollees pay no premium (other than the Part B premium) in 2019

Figure 5: Distribution

of Medicare Advantage Enrollees, by Prescription Drug Plan Premium, 2019

In 2019, 90% of Medicare Advantage plans offer

prescription drug coverage (MA-PDs), and most Medicare Advantage

enrollees (88%) are in plans that include this prescription drug coverage. More

than half of these beneficiaries (56%) pay no premium for their plan, other

than the Medicare Part B premium. However, 21 percent of beneficiaries in

MA-PDs (3.0 million enrollees) pay at least $50 per month, including 7 percent

who pay $100 or more per month, in addition to the monthly Part B premium

($135.50 in 2019). Among MA-PD enrollees who pay a premium for their plan, the

average premium is $65 per month. All together, including those who do not pay

a premium, the average MA-PD enrollee pays $29 per month in 2019.

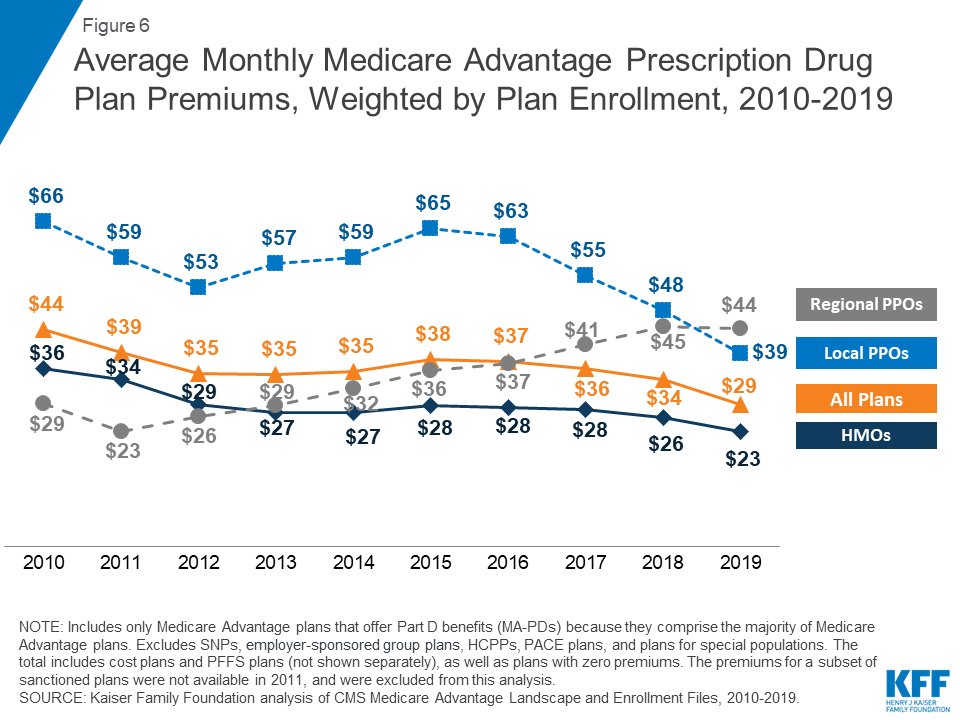

6. Premiums paid by Medicare

Advantage enrollees have slowly declined since 2015

Figure 6: Average

Monthly Medicare Advantage Prescription Drug Plan Premiums, Weighted by Plan

Enrollment, 2010-2019

Nationwide, average Medicare Advantage

Prescription Drug (MA-PD) premiums declined by $5 per month between 2018 and

2019, much of which was due to the relatively sharp decline in premiums for

local PPOs this past year, and since 2015. Average premiums for HMOs also

declined $3 per month, while premiums for regional PPOs were relatively similar

between 2018 and 2019. Average MA-PD premiums vary by plan type, ranging from

$23 per month for HMO enrollees to $39 per month for local PPO enrollees and

$44 per month for regional PPO enrollees. Nearly two-thirds (62%) of Medicare

Advantage enrollees are in HMOs, 31% are in local PPOs, and 6% are in regional

PPOs in 2019.

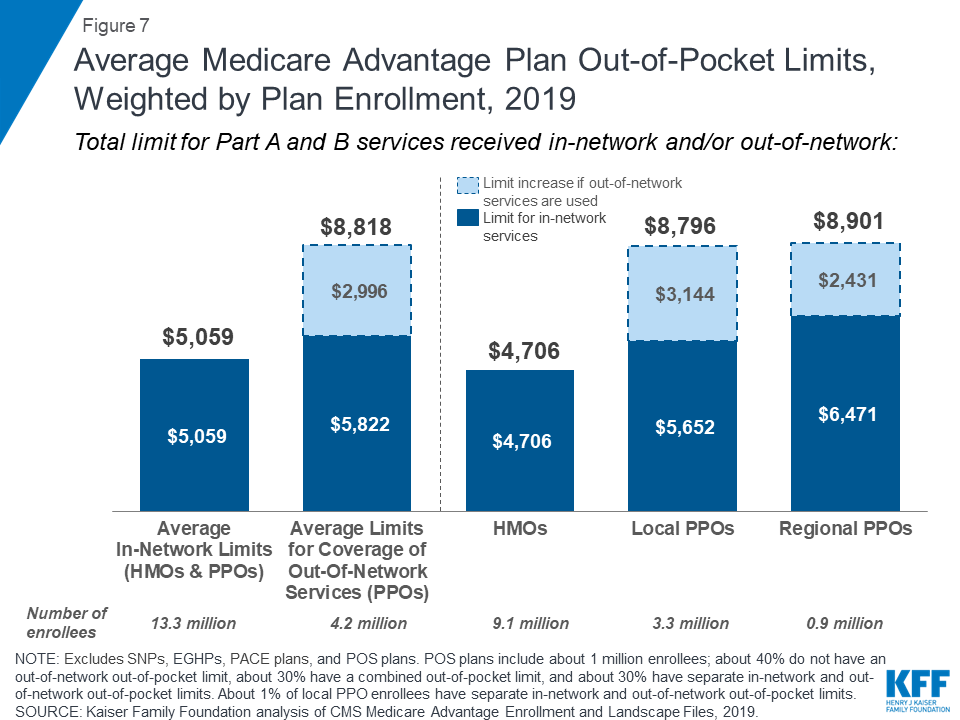

7. For Medicare

Advantage enrollees, the average out-of-pocket limit is $5,059 for in-network

services and $8,649 for both in-network and out-of-network services (PPOs)

Figure 7: Average

Medicare Advantage Plan Out-of-Pocket Limits, Weighted by Plan Enrollment, 2019

In 2019, Medicare Advantage enrollees’ average

out-of-pocket limit for in-network services is $5,059 (HMOs and PPOs) and

$8,818 for out-of-network services (PPOs). For HMO enrollees, the average

out-of-pocket (in network) limit is $4,706; these plans do not cover services

received from out-of-network providers. For local and regional PPO enrollees,

the average out-of-pocket limit for both in-network and out-of-network services

are $8,796, and $8,901, respectively.

Since 2011, the Administration has required

Medicare Advantage plans to provide an out-of-pocket limit for services covered

under Parts A and B not to exceed $6,700 (in-network) or $10,000 (in-network

and out-of-network combined). Limits have been required for regional PPOs since

2006.

HMOs generally only cover the services

provided by in-network providers, whereas PPOs also cover services delivered by

out-of-network providers but charge enrollees higher cost-sharing for this

care. The size of Medicare Advantage provider networks for physicians and hospitals vary

greatly both across counties and across plans in the same county.

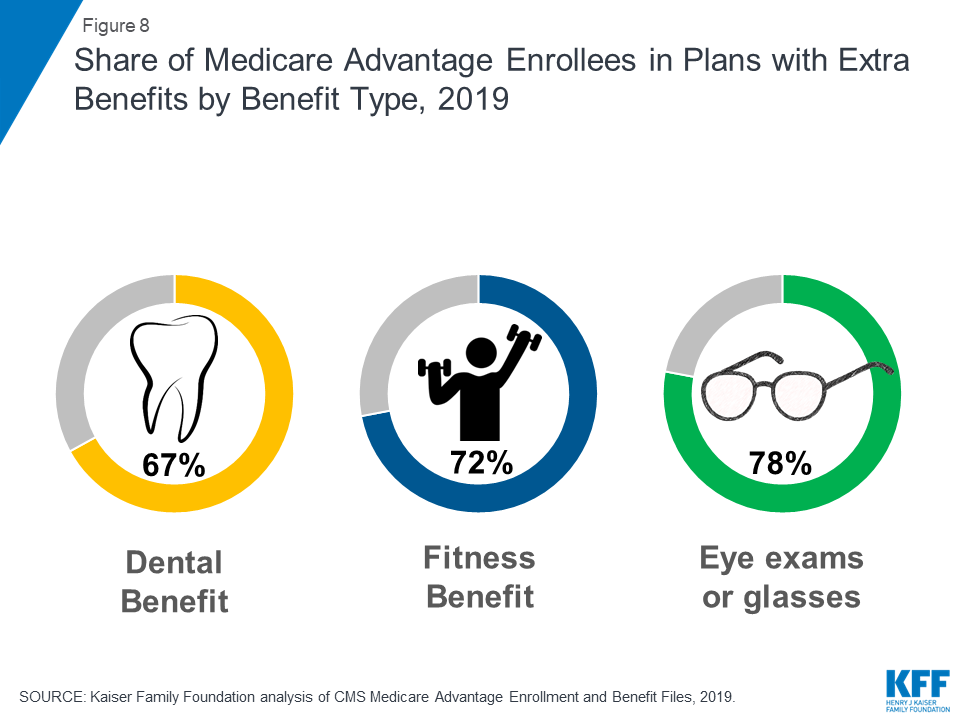

8. Most Medicare

Advantage enrollees have access to some benefits not covered by traditional

Medicare in 2019

Figure 8: Share of

Medicare Advantage Enrollees in Plans with Extra Benefits by Benefit Type, 2019

Medicare Advantage plans may provide extra

benefits that are not offered in traditional Medicare, and can use rebate

dollars to help cover the cost of extra benefits. Plans can also charge

additional premiums for such benefits. Most enrollees are in plans that provide

access to some dental care (67%), a

fitness benefit (72%), and/or eye exams or glasses (78%). Since 2010, the share

of enrollees in plans that provide some dental care or fitness benefits has

increased (from 48% and 52% of enrollees, respectively) while the share with a

vision benefit has been relatively steady (77% in 2010).

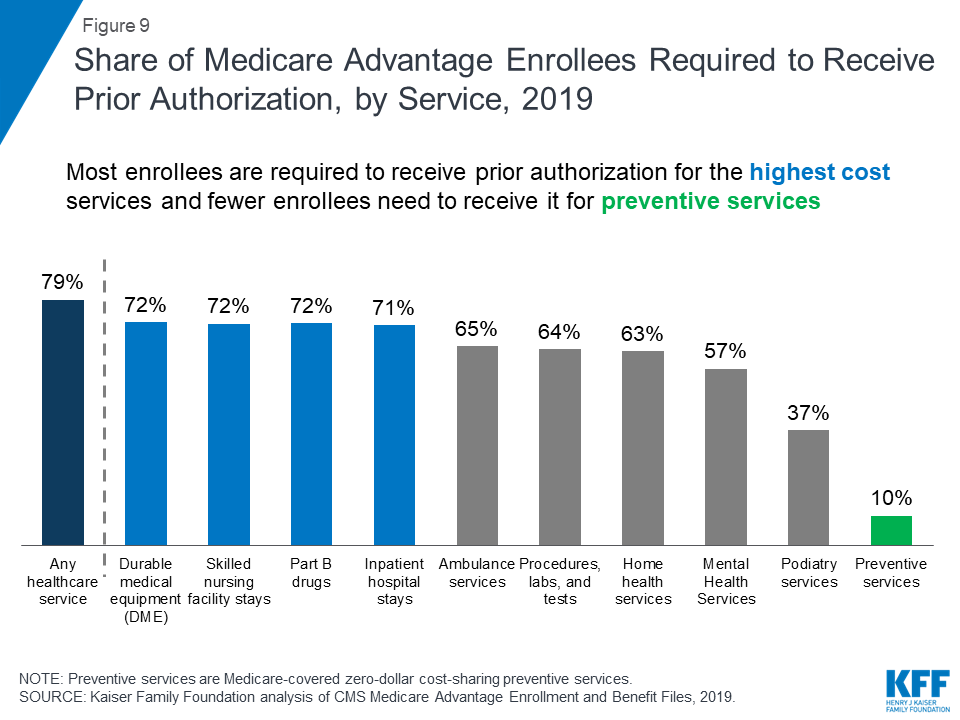

9. Nearly four out of

five Medicare Advantage enrollees are in plans that require prior authorization

for some services

Figure 9: Share of

Medicare Advantage Enrollees Required to Receive Prior Authorization, by

Service, 2019

Medicare Advantage plans can require enrollees

to receive prior authorization before a service will be covered, and nearly

four out of five Medicare Advantage enrollees (79%) are in plans that require

prior authorization for some services in 2019. Prior authorization is most

often required for relatively expensive services, such as inpatient hospital

stays, skilled nursing facility stays, and Part B drugs, but infrequently

required for preventive services. Beginning in 2019, Medicare Advantage plans

can also require enrollees to use “step therapy” for Part B drugs, meaning that

they are required to try some specific drugs (and fail to improve on those

drugs) before they receive approval to try other drugs. In contrast to Medicare

Advantage plans, traditional Medicare does not generally require prior

authorization for services, and does not require step therapy for Part B drugs.

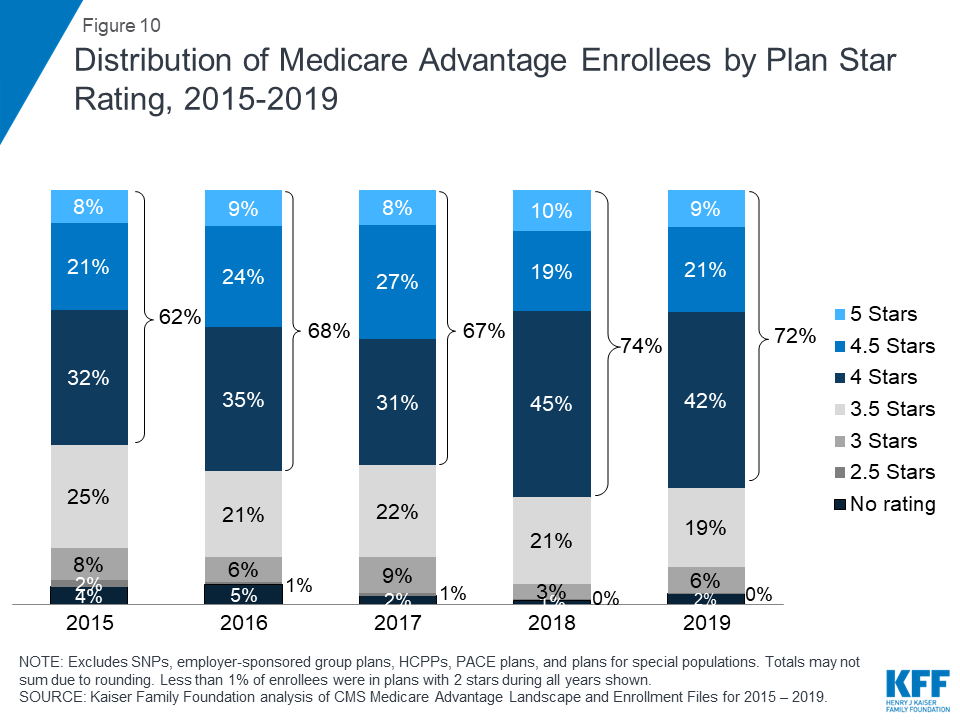

10. The majority (72%)

of Medicare Advantage enrollees are in plans that receive high quality ratings

(4 or more stars) and related bonus payments

Figure 10:

Distribution of Medicare Advantage Enrollees by Plan Star Rating, 2015-2019

In 2019, more than two-thirds (72%) of

Medicare Advantage enrollees are in plans with quality ratings of 4 or more

stars, a decrease from 74 percent in 2018. An additional 2 percent of enrollees

are in plans that were not rated because they were part of contracts that had

too few enrollees or were too new to receive ratings. Plans with 4 or more stars

and plans without ratings are eligible to receive bonus payments for each

enrollee the following plan year (2020). The share of enrollees in plans with

2.5 stars (below average ratings) nearly doubled from 3 percent in 2018 to 6

percent (nearly 1 million people) in 2019.

For many years, the Centers for Medicare and

Medicaid Services (CMS) has posted quality ratings of Medicare Advantage plans

to provide beneficiaries with additional information about plans offered in

their area. All plans are rated on a 1 to 5-star scale, with 1 star

representing poor performance, 3 stars representing average performance, and 5

stars representing excellent performance. CMS assigns quality ratings at the

contract level, rather than for each individual plan, meaning that each plan

covered under the same contract receives the same quality rating (and most

contracts cover multiple plans).

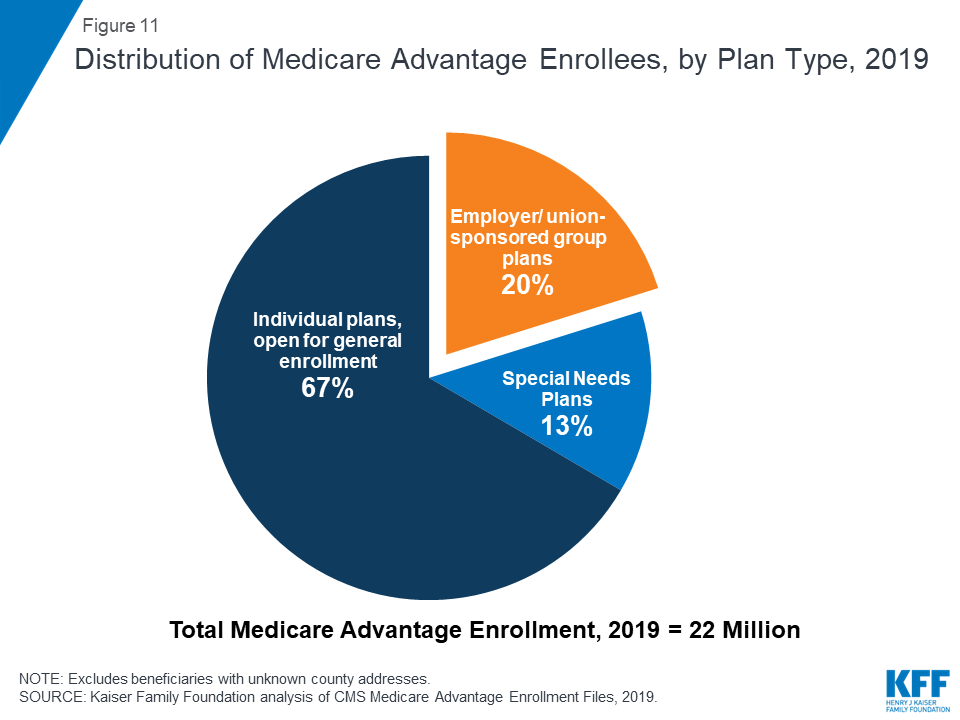

11. One in five

Medicare Advantage enrollees are in employer or union-sponsored group plans in

2019

Figure 11:

Distribution of Medicare Advantage Enrollees, by Plan Type, 2019

One in five Medicare Advantage enrollees (4.4

million) are in group plans offered by employers and unions for their retirees

in 2019. Under these arrangements, employers or unions contract with an insurer

and Medicare pays the insurer a fixed amount per enrollee to provide benefits

covered by Medicare. The employer or union (and sometimes the retiree) may also

pay a premium for additional benefits or lower cost-sharing. Group enrollees

comprise a disproportionately large share of Medicare Advantage enrollees in

ten states: Alaska (100%), West Virginia (50%), Michigan (49%), New Jersey

(42%), Illinois (39%), Kentucky (38%), Wyoming (37%), Maryland (36%), Delaware

(35%), and New Hampshire (33%).

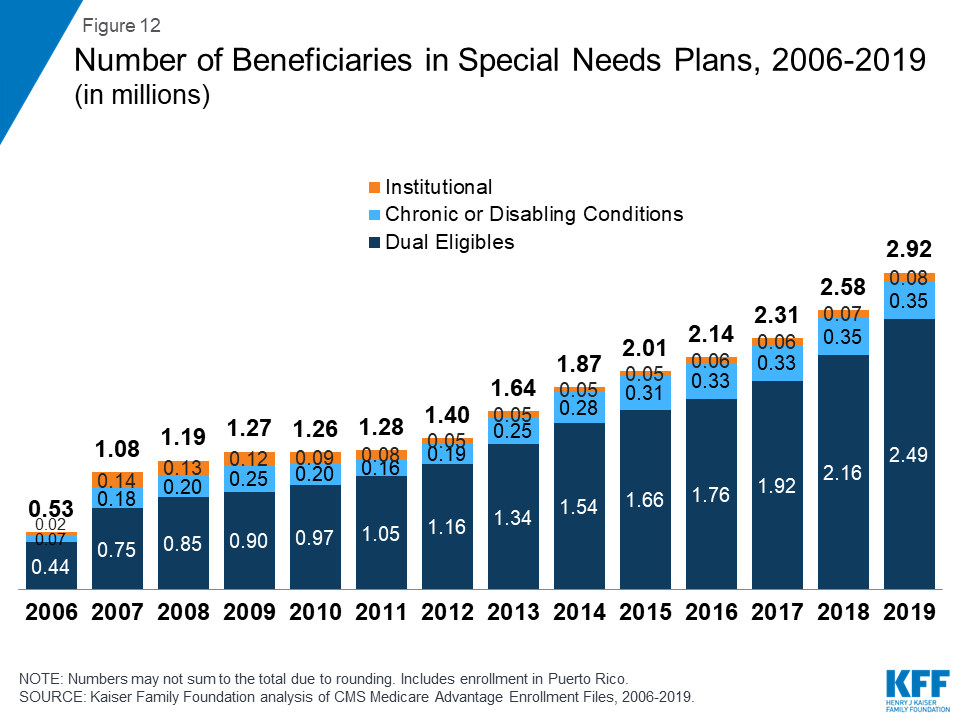

12. Nearly 3 million

Medicare beneficiaries are enrolled in Special Needs Medicare Advantage Plans

in 2019

Figure 12: Number of

Beneficiaries in Special Needs Plans, 2006-2019 (in millions)

Special Needs Plans (SNPs) restrict enrollment

to specific types of beneficiaries with significant or relatively specialized

care needs. The majority of SNP enrollees (85%) are in plans for beneficiaries

dually eligible for Medicare and Medicaid (D-SNPs), with the remainder in plans

for beneficiaries requiring a nursing home or institutional level of care

(I-SNPs), or with severe chronic or disabling conditions (C-SNPs.)

Enrollment in SNPs increased modestly from 2.6

million beneficiaries in 2018 to 2.9 million beneficiaries in 2019, accounting

for about 13 percent of total Medicare Advantage enrollment in 2019, with some

variation across states. In seven states, the District of Columbia, and Puerto

Rico, enrollment in SNPs comprises at least one-fifth of Medicare Advantage

enrollment (51% in DC, 49% in PR, 25% in SC, 22% in NY, 21% in AR, 20% in AZ,

20% in FL, 20% in GA, and 20% in TN). Most C-SNPs enrollees (93%) are in plans

for people with diabetes or cardiovascular disorders in 2019. Enrollment in

I-SNPs has been increasing, but is still less than 100,000 beneficiaries.

Gretchen Jacobson, Meredith Freed, and Tricia

Neuman are with KFF.

Anthony Damico is an independent consultant.

Anthony Damico is an independent consultant.

|

Data and Methods

This analysis uses

data from the Centers for Medicare and Medicaid Services (CMS) Medicare

Advantage Enrollment, Benefit and Landscape files for the respective year,

with enrollment data from March of each year. Cost plans are grouped with

Medicare Advantage plans, and this chart collection uses the term Medicare

Advantage to refer to both types of plans, even though cost plans are paid

differently and subject to different rules.

|

No comments:

Post a Comment