Meredith Freed , Jeannie Fuglesten Biniek Follow @jeanniebin on

Twitter , Anthony Damico , and Tricia Neuman Follow @tricia_neuman on

Twitter Published: Jun 21, 2021

Medicare beneficiaries have the option of

receiving their Part A and Part B Medicare benefits through a private Medicare

Advantage plan. Since 2011, the federal government has required Medicare

Advantage plans to cap out-of-pocket spending, and these plans may provide

additional benefits or reduced cost sharing compared to traditional Medicare.

They are also permitted to limit provider networks, may require prior

authorization for certain services, and sometimes carry an additional premium

on top of the monthly Part B premium all Medicare beneficiaries pay. This brief

provides current information about Medicare Advantage premiums, cost sharing,

out-of-pocket limits, and supplemental benefits, as well as trends over time.

Two companion analyses examine trends in Medicare Advantage enrollment and Medicare Advantage plans’ star ratings and federal spending under the

quality bonus program.

Nearly two-thirds of Medicare Advantage

enrollees pay no supplemental premium (other than the Part B premium) in 2021

In 2021, 89% of individual Medicare Advantage plans offer prescription drug

coverage (MA-PDs), and most Medicare Advantage enrollees (90%) are

in plans that include this prescription drug coverage. Nearly two-thirds of

beneficiaries in individual Medicare Advantage plans with prescription drug

coverage (65%) pay no premium for their plan, other than the Medicare Part B

premium ($148.50 in 2021). However, 15% of beneficiaries in individual MA-PDs

(2.6 million enrollees) pay at least $50 per month, including 5% who pay $100

or more per month, in addition to the monthly Part B premium. The MA-PD premium

includes both the cost of Medicare-covered Part A and Part B benefits and Part

D prescription drug coverage. Among the one-third of all enrollees in an

individual MA-PD who pay a premium for their plan (6.0 million enrollees), the

average premium is $60 per month. Altogether, including those who do not pay a

premium, the average individual MA-PD enrollee pays $21 per month in 2021.

Premiums paid by Medicare Advantage enrollees

have declined slowly since 2015

Average Medicare Advantage Prescription Drug

(MA-PD) premiums declined by $4 per month between 2020 and 2021, much of which

was due to the relatively sharp decline in premiums for local PPOs, which fell

by $7 per month. Since 2016, enrollment in local PPOs has increased rapidly as

a share of all Medicare Advantage enrollment, corresponding to broader availability of these plans. Average premiums for HMOs

declined $2 per month, while premiums for regional PPOs increased $1 per month

between 2020 and 2021.

Average MA-PD premiums vary by plan type,

ranging from $18 per month for HMOs to $25 per month for local PPOs and $48 per

month for regional PPOs. For all MA-PDs, the monthly premium is $21 per month

for both Part A and Part B benefits and Part D prescription drug coverage (and

averages $12 for just the Part D portion of covered benefits). Nearly

two-thirds (60%) of Medicare Advantage enrollees are in HMOs, 35% are in local

PPOs, and 4% are in regional PPOs in 2021.

Slightly more than half of all Medicare

Advantage enrollees would incur higher costs than beneficiaries in traditional

Medicare for a 6-day hospital stay

Medicare Advantage plans have the flexibility

to modify cost sharing for most services, subject to limitations. Total

Medicare Advantage cost sharing for Part A and B services cannot exceed cost

sharing for those services in traditional Medicare on an actuarially equivalent

basis. Further, Medicare Advantage plans may not charge enrollees higher cost

sharing than under traditional Medicare for certain specific services,

including chemotherapy, skilled nursing facility (SNF) care, and renal dialysis

services.

However, Medicare Advantage plans may reduce

cost sharing as a mandatory supplemental benefit, and may use rebate dollars to

do so. According to the Medicare Payment Advisory Commission (MedPAC), in 2021,

about 46 percent of rebate dollars were used to lower cost

sharing for Medicare services.

In the case of inpatient hospital stays,

Medicare Advantage plans generally do not impose the Part A deductible, but

often charge a daily copayment, beginning on day 1. Plans vary in the number of

days they impose a daily copayment for inpatient hospital care, and the amount

they charge per day. In contrast, under traditional Medicare, when

beneficiaries require an inpatient hospital stay, there is a deductible of $1,484 in 2021 (for one spell of illness) with

no copayments until day 60 of an inpatient stay (assuming no supplemental

coverage that covers some or all of the deductible).

In 2021, virtually all Medicare Advantage

enrollees (99%) would pay less than the traditional Medicare Part A hospital

deductible for an inpatient stay of 3 days, and these enrollees would pay $747

on average (Figure 3). But slightly more than half of all Medicare Advantage

enrollees (53%) would pay more than they would under traditional Medicare (with

its $1,484 deductible) for stays of 6 or more days, with average cost sharing

of $1,763, among those enrollees with costs above traditional Medicare.

For a stay of 10 days, 69% of Medicare

Advantage enrollees would pay more than beneficiaries in traditional Medicare,

and among those enrollees in plans with cost-sharing requirements that would

exceed the Part A deductible, average cost sharing would be $2,059. For a

length of stay of a least 20 days, 81% of Medicare Advantage enrollees would

pay more in cost sharing than the Part A deductible – $4,866 on average.

This analysis does not take into account the

fact that a majority of people in traditional Medicare would not pay the

deductible if hospitalized because they have supplemental coverage, although

those with Medigap or retiree health would have the additional cost of a

monthly premium. However, 5.6 million beneficiaries in traditional Medicare have no supplemental

coverage and would be liable for the full Part A deductible if

admitted to the hospital.

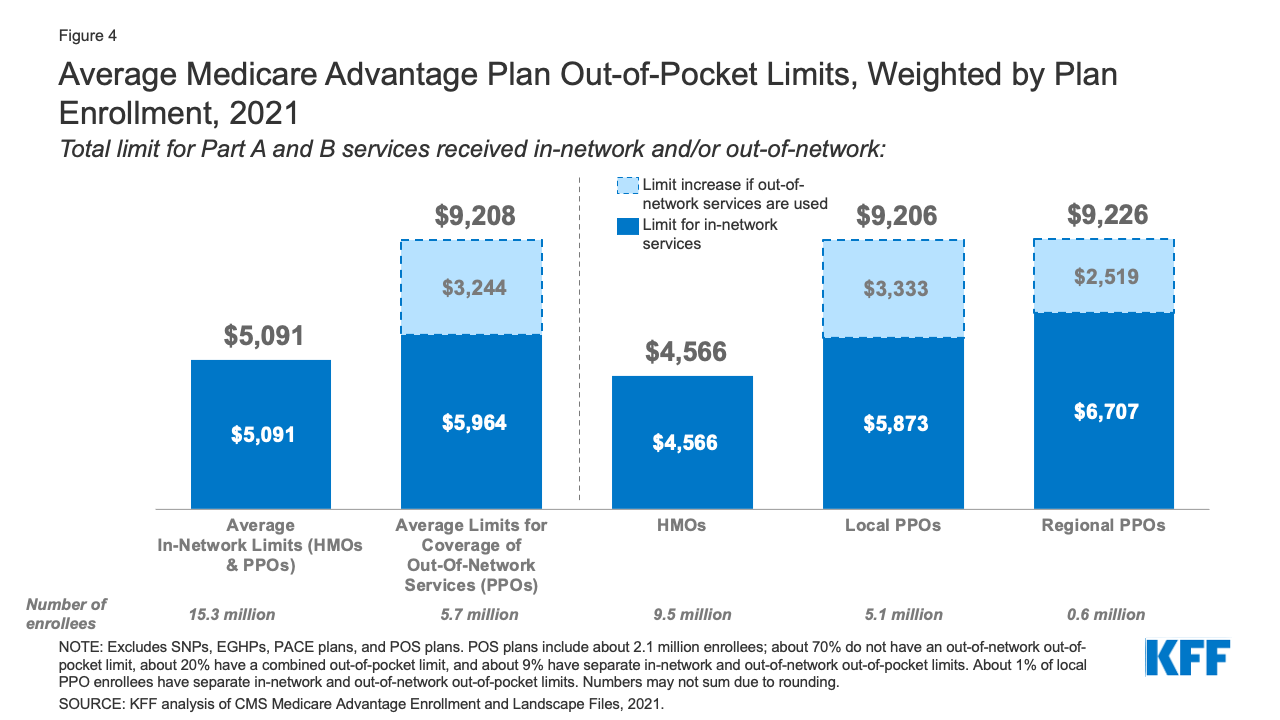

The average out-of-pocket limit for Medicare

Advantage enrollees is $5,091 for in-network services and $9,208 for both

in-network and out-of-network services (PPOs)

Figure 4: Average Medicare Advantage Plan

Out-of-Pocket Limits, Weighted by Plan Enrollment, 2021

Since 2011, federal regulation has required

Medicare Advantage plans to provide an out-of-pocket limit for services covered

under Parts A and B. In 2021, the out-of-pocket limit may not exceed $7,550 for

in-network services and $11,300 for in-network and out-of-network services

combined. These out-of-pocket limits apply to Part A and B services only, and

do not apply to Part D spending, for which there is a separate out-of-pocket threshold of $6,550 in 2021,

above which enrollees pay 5% of costs. Whether a plan has only an in-network

cap or a cap for in- and out-of-network services depends on the type of plan.

HMOs generally only cover services provided by in-network providers, whereas

PPOs also cover services delivered by out-of-network providers but charge enrollees

higher cost sharing for this care. The size of Medicare Advantage provider

networks for physicians and hospitals vary greatly both across counties and across

plans in the same county.

In 2021, the weighted average out-of-pocket

limit for Medicare Advantage enrollees is $5,091 for in-network services and

$9,208 for in-network and out-of-network services combined. For enrollees in

HMOs, the average out-of-pocket (in-network) limit is $4,566. Enrollees in HMOs

are generally responsible for 100% of costs incurred for out-of-network care.

However, HMO point of service (POS) plans allow out-of-network care for certain

services, though it typically costs more than in-network coverage. For local

and regional PPO enrollees, the average out-of-pocket limit for both in-network

and out-of-network services is $9,206, and $9,226, respectively.

The average out-of-pocket limit for in-network

services has generally trended down from 2017 but increased slightly between

2020 to 2021. The average in-network limit for HMOs increased from $4,925 in

2020 to $5,091 in 2021. The average combined in- and out-of-network limit for

PPOs increased from $8,828 in 2020 to $9,208 in 2021.

Most Medicare Advantage enrollees have access

to some benefits not covered by traditional Medicare in 2021 and special needs

plan (SNP) enrollees have greater access to certain benefits

Medicare Advantage plans may provide extra

(“supplemental”) benefits that are not available in traditional Medicare. The

cost of these benefits may be covered using rebate dollars (which may include

bonus payments) paid by CMS to private plans. In recent years, the rebate

portion of federal payments to Medicare Advantage plans has risen

rapidly, totaling $140 per enrollee per month in 2021, a 14% increase over 2020.

Plans can also charge additional premiums for such benefits. Beginning in 2019,

Medicare Advantage plans have been able to offer additional supplemental

benefits that were not offered in previous years. These supplemental benefits

must still be considered “primarily health related” but CMS expanded this

definition, so more items and services are available as supplemental benefits.

Most enrollees in individual Medicare

Advantage plans (those generally available to Medicare beneficiaries) are in

plans that provide access to eye exams and/or glasses (99%), telehealth

services (94%), dental care (94%), a fitness benefit (93%), and hearing

aids (93%). Similarly, most enrollees in SNPs are in plans that provide access

to these benefits. This analysis excludes employer-group health plans because

employer plans do not submit bids, and data on supplemental benefits may not be

reflective of what employer plans actually offer.

Though these benefits are widely available,

the scope of specific services varies. For example, a dental benefit may

include preventive services only, such as cleanings or x-rays, or more comprehensive

coverage, such as crowns or dentures. Plans also vary in terms of cost sharing

for various services and limits on the number of services covered per year and

many impose an annual dollar cap on the amount the plan will pay toward covered

services. Enrollees in SNPs have more access to certain benefits compared to

enrollees in individual plans, such as over the counter drug benefits (97% vs

79%); transportation (88% vs 37%); a meal benefit (73% vs 55%) and in-home

support services (14% vs 7%). However, there is no publicly available data on

how frequently supplemental benefits are utilized by enrollees or the amounts

they pay out-of-pocket for these services.

As of 2020, Medicare Advantage plans have been

allowed to include telehealth benefits as part of the basic benefit package

– beyond what was allowed under traditional Medicare prior to the public

health emergency. These benefits are considered “telehealth” in the

figure above, even though their cost may not be covered by either rebates or

supplemental premiums. Additionally, Medicare Advantage plans may also offer

supplemental telehealth benefits via remote access technologies and/or

telemonitoring services, which can be used for those services that do not meet

the requirements for coverage under traditional Medicare or the requirements

for additional telehealth benefits (such as the requirement of being covered by

Medicare Part B when provided in-person). The majority of enrollees in both

individual plans and SNPs have access to remote access technologies (70% and

79%, respectively), but just 5% of enrollees in individual plans and 6% of

enrollees in SNPs have access to telemonitoring services.

Nearly all Medicare Advantage enrollees are in

plans that require prior authorization for some services

Medicare Advantage plans can require enrollees

to receive prior authorization before a service will be covered, and nearly all

Medicare Advantage enrollees (99%) are in plans that require prior

authorization for some services in 2021. Prior authorization is most often

required for relatively expensive services, such as inpatient hospital stays,

Part B drugs, and skilled nursing facility stays, and is rarely required for

preventive services. Prior authorization is also required for the majority of

enrollees for some extra benefits (in plans that offer these benefits),

including comprehensive dental services, hearing and eye exams, and

transportation. The number of enrollees in plans that require prior

authorization for one or more services stayed the same from 2020 to 2021. In

contrast to Medicare Advantage plans, traditional Medicare does not generally

require prior authorization for services and does not require step therapy for

Part B drugs.

Discussion

In 2021, nearly two-thirds of Medicare

Advantage enrollees are in plans that do not charge a premium (other than the

Part B premium), although the remaining third do pay an additional premium,

averaging about $60 per month. Most enrollees are in plans that provide access

to a variety of supplemental benefits, such as eye exams, dental and fitness

benefits. Nearly all enrollees are in plans that require prior authorization

for some services. Medicare Advantage cost sharing varies across plans and can

be lower than traditional Medicare, but that is not always the case. Slightly

more than half of all Medicare Advantage enrollees would incur higher costs

than beneficiaries in traditional Medicare with no supplemental coverage for a

6-day hospital stay, though cost are generally lower in Medicare Advantage for

shorter stays.

While data on Medicare Advantage plan

availability and enrollment and plan offerings is robust, the same cannot be

said about service utilization and out-of-pocket spending patterns, which is essential

for assessing how well the program is meeting its goals in terms of value and

quality and to help Medicare beneficiaries compare coverage options. As

enrollment in Medicare Advantage and federal payments to private plans

continues to grow, this information will become increasingly important.

Meredith Freed, Jeannie Fuglesten Biniek, Tricia Neuman are with

KFF. Anthony Damico is an independent consultant.

|

Methods |

|

This analysis uses data from

the Centers for Medicare & Medicaid Services (CMS) Medicare Advantage

Enrollment, Benefit and Landscape files for the respective year. KFF is now

using the Medicare Enrollment Dashboard for enrollment data, from March of

each year. This analysis uses the term Medicare

Advantage to refer to Medicare Advantage plans and other types of private

plans, including cost and PACE plans. However, MMPs are excluded from this

analysis. Enrollment counts in publications by firms operating in the Medicare

Advantage market, such as company financial statements, might differ from KFF

estimates due to inclusion or exclusion of certain plan types, such as SNPs

or employer plans. For calculating how much Medicare

beneficiaries could pay out-of-pocket for an inpatient hospital admission, we

used the 2021 Medicare Plan Finder Benefit Summary data. For traditional

Medicare, beneficiaries without supplemental coverage would incur the Part A

hospital deductible of $1,484 in 2021 (for one spell of illness). For

Medicare Advantage, we use 2021 Medicare Plan Finder data to calculate

out-of-pocket costs for inpatient stays for Medicare Advantage enrollees,

weighted by 2021 plan enrollment. The analysis does not take into account

deductibles that some Medicare Advantage enrollees face, and if taken into

account, would increase costs for some enrollees. The analysis also does not

take into account maximum out-of-pocket limits under Medicare Advantage,

which would cap the amount enrollees pay for their care, including

hospitalizations. It is possible that some Medicare Advantage enrollees would

reach their out-of-pocket limit during their inpatient stay, particularly if

they had incurred high expenses prior to an inpatient admission. However, in

2021 the average out-of-pocket maximum is $5,091, which is above the

cost-sharing amount that all Medicare Advantage enrollees would pay for a

6-day hospital stay, assuming no other medical expenses during the coverage

year. |

No comments:

Post a Comment