Tara O'Neill Hayes January 25, 2019

Executive Summary

- A Wall Street Journal report details

how private insurers that offer plans through Medicare Part D are

leveraging the program’s structure to contain their losses and increase

their profits, resulting in $9.1 billion in extra subsidies.

- Medicare Part D’s costs are rising for a number of

reasons, primarily as a result of an increase in spending in the

“catastrophic” phase of the insurance plans—the area of the program that

insurers are using to contain their losses.

- The

existing evidence on the program’s rising costs and misaligned incentives,

including the Journal’s report, demonstrates the importance of

restructuring the program to realign incentives for all stakeholders. One

such proposal is detailed here.

Introduction

A recent Wall Street Journal investigative

report made a dramatic claim in its headline: “The $9 Billion Upcharge—How Insurers Kept Extra Cash From

Medicare.” In this article, the Journal examines

how insurers set Medicare Part D premiums so as to increase the likelihood that

they will earn a profit on those plans at the expense of federal taxpayers.

The Medicare Part D program provides Medicare

beneficiaries with access to subsidized outpatient prescription drug coverage

through private insurance plans, and the program’s costs are rising. In 2018,

43.9 million seniors (or 73 percent of all Medicare beneficiaries) enrolled in

Part D, and enrollment—and therefore cost—is expected to increase each year for

the foreseeable future.[1] These

rising program costs have raised concerns among policymakers, and the Journal report

highlighted one area of concern: reinsurance.

The federal government covers most of the costs

in the final, “catastrophic” phase of Part D coverage—the reinsurance phase.

The recent exposé depicts insurers as exploiting the reinsurance structure to

guard against losses while using another aspect of the program’s structure—risk

corridors—to boost their profits illegitimately. Yet in structuring their plans

the way they are, insurers are legally and rationally responding to the

program’s incentives. To stop this practice and contain costs more broadly

within the Medicare Part D program requires reforms to the program’s structure.

One such reform option is outlined below.

Rising Reinsurance Costs

Overall program expenditures grew at an average

annual rate of 6 percent between 2007 and 2016, almost exclusively as a result

of rising reinsurance expenditures. The program’s rising reinsurance costs are

a function of both continued growth in the number of beneficiaries who reach

the catastrophic threshold as well as continued growth in the amount of

spending for each of those enrollees. Expenditures for such high-cost enrollees

rose at an annual rate of 10.4 percent between 2010 and 2015; in contrast,

average expenditures for the remainder of enrollees actually declined by an

average of 2.1 percent each year during that period.[2] Consequently,

spending above the catastrophic threshold has also been rising more rapidly

over this period relative to before 2010: 26.6 percent compared with 12 percent

previously.[3] Ultimately,

high-cost enrollees accounted for 57 percent of program expenditures in 2015,

despite being only 28 percent of beneficiaries.[4]

The growth in the cost of high-cost enrollees

not only increases the federal government’s cost to

subsidize the program, but also changes how the federal

government subsidizes the program. This rising spending has led to a dramatic

increase in the share of the federal government’s subsidy being paid through

reinsurance rather than premium subsidies: Reinsurance payments accounted for

less than one-third (31 percent) of the federal government’s share of the

program’s cost in 2007, but more than two-thirds of the cost in 2016 (68

percent).[5]

While the program has been largely successful, these and other trends over

the past several years have highlighted the need for structural reforms to

eliminate perverse incentives.

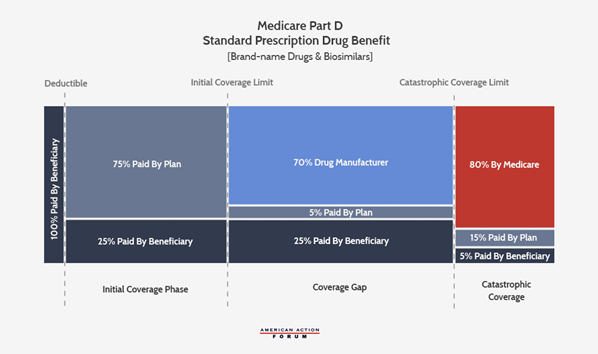

Understanding Medicare Part D’s Structure

Medicare Part D Bids

In order to participate in the program and

receive government subsidies for the coverage offered, Part D plan sponsors

(i.e. insurers) must submit a bid to the Centers for Medicare

& Medicaid Services (CMS) estimating their cost to provide the plan’s

covered benefits for each enrollee. Specifically, a sponsor’s bid reflects the

estimated cost of providing the “basic benefit” to an average beneficiary plus,

if it chooses, the estimated cost of any supplemental or enhanced benefits.[6] The

cost of the basic benefit is based on the plan’s required liability under each

phase of coverage, as shown in the chart below—including plans’ 15 percent

liability in the catastrophic phase.[7]

The Government Subsidy

The government subsidy has two components: the

direct subsidy of the premium and the reinsurance subsidy of excess

catastrophic costs. The direct subsidy covers 74.5 percent of the national

average bid for the basic benefit; it is paid to plans each month and does not

change throughout the year. Enrollees cover the difference between the direct

subsidy and the premium. If an enrollee chooses a plan with a

lower-than-average bid, they may not have to pay any premium, whereas enrollees

in plans with a higher-than-average bid will have to pay a larger premium.

If a plan’s costs for providing the basic

benefit are above or below their estimated costs, the direct subsidy payments

are reconciled with the plan’s actual costs at the end of the year—but only

under certain circumstances, as discussed below in the “Risk Corridors”

section. The circumstances create the room that insurers are using to make more

money, as the Journal reported.

The reinsurance subsidy covers 80 percent of

costs over the catastrophic coverage threshold beyond the amounts estimated in

the bid for the basic benefit. Unlike the direct subsidy, the reinsurance

subsidy is always reconciled with actual costs such that plans are protected

from ever having to pay more than 15 percent of each beneficiary’s catastrophic

costs.

The total government subsidy is supposed to

cover 74.5 percent of the program’s costs; however, this percentage is not set

in law.

Risk Corridors

When Congress and the Bush Administration were

creating Part D, there was concern among policymakers that few insurers would

offer plans because they would struggle to predict costs, and thus they would

face a substantial potential to lose money. Simply, if a plan’s actual costs

were more than expected, the direct subsidy payment would not cover as much of

their costs as intended; alternatively, if a plan’s actual costs were less than

estimated, the subsidy would be more than needed and the plan sponsor would

gain a profit. Accordingly, a risk corridor program was included to guard against

substantial financial losses while also preventing equally substantial profits

at the expense of beneficiaries and taxpayers.

The risk corridor established limits on both

financial gains and losses for a plan. If a plan’s actual costs for the basic

benefit are within five percent in either direction of the sponsor’s estimated

costs, there is no reconciliation of direct subsidy payments: The plan is

responsible for all the loss it incurs or may keep all of the additional

subsidy payments as profit. If a plan’s actual costs are more than 5 percent

but less than 10 percent above or below the sponsor’s bid, the first 5 percent

is treated the same, and the portion of loss or profit between 5 percent and 10

percent is split between the plan and Medicare 50/50. Similarly, if a plan’s

costs differ from the bid by more than 10 percent, the initial 10 percent is

treated as just described and the plan is responsible for 20 percent of the

losses over 10 percent if costs are higher than expected (or may keep 20

percent of the savings from the higher-than-needed direct subsidy payments over

10 percent). The following chart from the Medicare Payment Advisory Commission

(MedPAC) provides a helpful visual.[8]

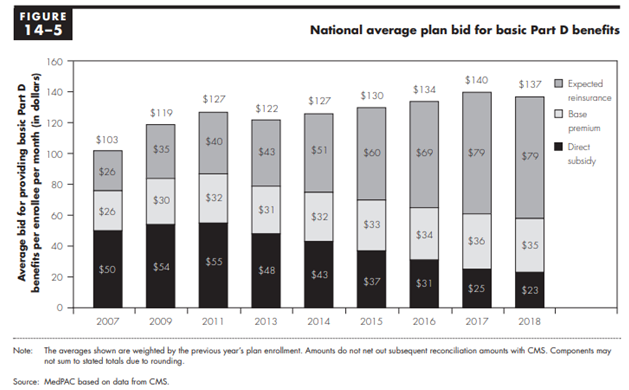

The Impact: Why This Matters

Government Subsidy of Part D Increasingly

Consumed by Reinsurance

As noted, the growth in Part D spending is the

result of continued increases in both the number of high-cost enrollees and the

total amount spent for each of those high-cost enrollees. The program’s own

structure, however, has allowed for a third factor to increase program costs.

The federal government is supposed to cover 74.5

percent of all program costs (excluding beneficiary cost-sharing, Low-Income

Subsidy cost-sharing subsidies, and the coverage gap rebates), and that

percentage must be split between the direct premium subsidy, the additional

low-income premium subsidies, and the reinsurance costs. In order for this

percentage to remain fixed, the federal government’s direct premium subsidies

must decrease as reinsurance costs increase. This cost-shifting can be seen in

the following chart from MedPAC’s March 2018 Report to Congress, showing the

government’s declining direct subsidy of the premiums and increasing

reinsurance subsidies, as well as the base premium paid by beneficiaries.[9]

Because of the existence and nature of the risk

corridors along with the fact that this overall subsidy rate is not set in law,

the federal government has actually covered more than 74.5 percent of the

program’s costs in most years.[10] That

is, the structure and limited application of the risk corridors to the direct

subsidy payments allows plan sponsors to underestimate their catastrophic

coverage expenditures and be made whole for most of their additional costs,

while simultaneously overestimating their other expenditures without having to

pay back all of the excess premium subsidies. The result is that rising

catastrophic costs spill into rising overall program costs.

The Latest Findings

While MedPAC had previously noted the

possibility for plans to design their bids in such a way, they were unable to

find specific evidence of such behavior; MedPAC noted that to the extent such

behavior was occurring, it was likely limited. The Wall

Street Journal, however, found evidence that insurers were in fact using

these allowances to minimize the threat of financial losses and maximize gains.

Part D plan sponsors overestimated their basic benefit costs, and as a result

of the risk corridors they were able to keep an additional $9.1 billion beyond

what they would have if they had accurately estimated their costs.[11] On

the other hand, plan sponsors also underestimated their reinsurance costs by

$27.8 billion from 2006-2015, and Medicare reimbursed plans for all of these

additional costs.

The Need for Reform (And How to Do It)

In structuring their bids this way, the

insurers’ behavior is both fully legal and the rational result of the

incentives established by the program’s structure. If policymakers find this

behavior to be undesirable, they should change the program to eliminate the

incentives to behave this way.

One way to alter incentives would be to increase

plan sponsors’ liability in the catastrophic coverage phase. AAF has previously

proposed this and other comprehensive reforms of the Part D program. Those

proposals are detailed here. The aim of this proposal is to realign

the incentives of plan sponsors with those of the beneficiaries and taxpayers

in order to bring down program costs for all parties. This proposal includes

the introduction of a cap on beneficiary out-of-pocket costs, moving mandatory

drug manufacturer rebates to the catastrophic phase, and increasing insurers’

liability in the catastrophic phase while reducing the government’s reinsurance

liability.

CMS has also just proposed a new voluntary demonstration program for

the Part D program that attempts to address the issue of rising reinsurance

costs. Under this demo, Part D plan sponsors would take on increased liability

in the catastrophic coverage phase in exchange for the possibility of shared

savings. CMS would determine the expected expenditure rate absent the demo and

plans would be able to share in any savings below the expected expenditure

amount; plans would also be liable for additional costs if expenditures

exceeded the expected rate.

Current trends and projections, including the

drugs currently in development and their expected costs, all indicate that the

need for reform will continue to grow.

[1] https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/ReportsTrustFunds/Downloads/TR2018.pdf

[6] A risk adjustment program is used to

increase or decrease payments to plans based on an enrollee’s health to

mitigate any additional costs that may be incurred if enrollees are sicker than

average or vice versa.

[7] Plans may choose different benefit designs

with varying degrees of liability, but any variation must still be actuarially

equivalent to this standard benefit design.

[8] Chart from MedPAC June 2015 report, Chapter 6. Edited for

space, eliminating the visual of the structure of the risk corridors in 2006

and 2007.

[11] https://www.wsj.com/articles/the-9-billion-upcharge-how-insurers-kept-extra-cash-from-medicare-11546617082

https://www.americanactionforum.org/insight/evidence-for-structural-reform-part-d/#ixzz5ddAoDpTm

Follow @AAF on Twitter

No comments:

Post a Comment