Tara O'Neill Hayes, Josee Farmer April 2, 2020

Executive Summary

·

Diabetes cost the United

States $327 billion in 2017, becoming the most expensive chronic disease in the

nation.

·

Insulin costs, before

accounting for any rebates or discounts, comprise an estimated $48 billion (20

percent) of the direct costs of treating diabetes; after rebates, insulin

accounts for 6.3 percent of costs.

·

The average list price

of insulin increased 11 percent annually from 2001 to 2018, with average annual

per capita insulin costs now nearing $6,000. Because patients’

out-of-pocket costs are typically based on list price, their expenses have

risen substantially despite the decrease in net price for many of the most

commonly used insulin products over the past several years.

·

If the trends of the

past decade continue, gross insulin costs in the United States could reach

$121.2 billion in total spending (or $12,446 per insulin patient) by 2024, but

if more recent trends of much slower price growth prevail, insulin spending

could total $60.7 billion in 2024 (or $6,263 per patient).

The Rising Cost of Diabetes

Diabetes is now the most expensive chronic

condition in the United States.[1] One in every four U.S. health care

dollars is spent on someone with diabetes, and one in seven dollars is spent

directly on diabetes-related expenses.[2] The

economic cost of diabetes in the United States totaled $327 billion in 2017,

including $237 billion for direct medical costs and $90 billion in lost

productivity.[3] The 2017 total represents an average

annual increase of 6 percent from the 2012 estimated cost of $245 billion.[4]

The rising costs of diabetes largely tracks the

dramatic increase in the cost of prescription

insulin—which an estimated 8.3 million individuals use to control

their condition. Between 2012 and 2018, the price of available insulin

increased 14 percent annually, on average, and in 2016 insulin accounted for 31

percent of a Type 1 diabetic’s health care costs, up from 23 percent in 2012.[5] The rising cost of insulin has an

impact on both patients and society as a whole. One fourth of diabetic

patients, no longer able to afford their prescribed treatment plans, ration

their supply, which can be dangerous and potentially fatal.[6] And nearly three-fifths (57 percent)

of individuals with diagnosed diabetes are insured through a public program,

such as Medicare, Medicaid, or the Children’s Health Insurance Program (CHIP),

and these programs cover a disproportionate share (66 percent) of the costs of

diabetes.[7] In other words, taxpayers end up

footing most of the bill for diabetes treatments.

Given the rising costs, it is worth

understanding what is driving these increases. This analysis first details

increases in insulin prices and offers a projection for how much insulin will

cost in the coming years. It then examines what is driving these increases.

The Price of Insulin

Past Price Growth

Since 1991, growth in insulin prices has been

accelerating, with a reprieve only in recent years. The list price of insulin

per milliliter in the United States increased, on average, 2.9 percent annually

from 1991-2001, 9.5 percent per year from 2002 and 2012, 20.7 percent annually

between 2012 and 2016, and 1.5 percent per year from 2016-2018.[8] .[9]

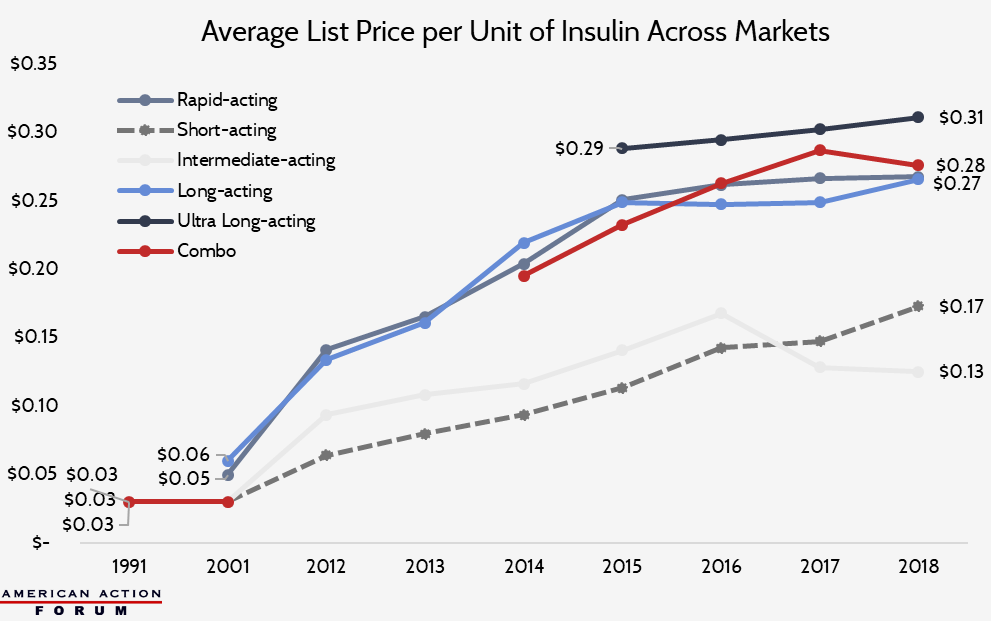

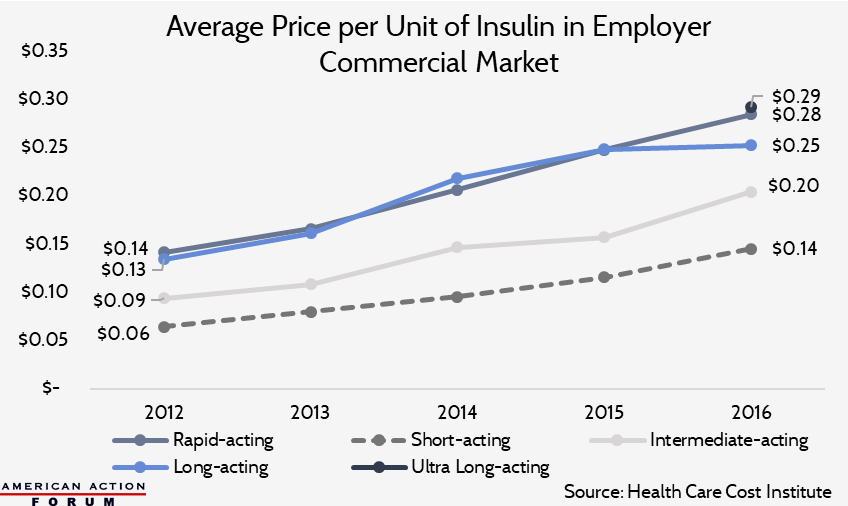

As the chart below shows, however, these

increases are driven not simply by price hikes for existing products, but by

higher prices for new products. Newer insulin products are more expensive than

older products. Since rapid-acting and long-/ultra-long-acting insulins are now

the most commonly used insulins, the rising cost of these medicines is

contributing significantly to rising average insulin costs per patient and

overall insulin spending.

The prices detailed above are list prices—and

the discrepancy between list prices and net prices due to rebates is likely

partially responsible for high insulin prices, as detailed below.

Insulin Spending in Medicaid

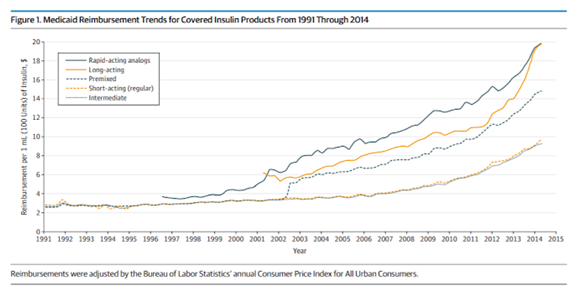

Examining Medicaid reimbursement for insulin

provides a useful window into market prices for insulin, as Medicaid, by law,

receives the “best price”

in the nation for all outpatient drugs. Medicaid reimbursements for insulin

have increased dramatically over the past decade. The chart below shows the

growth in the Medicaid reimbursement rate per milliliter (which typically

contains 100 units) of the various types of insulin. While the cost growth from

1991 to 2001 is noticeable, the increases from 2001 to 2014 were more rapid,

increasing an average of 9.1 percent annually primarily due to the introduction

of new insulin products.[10] These

price increases have resulted in Medicaid spending on insulin reaching $3.9

billion in 2018.[11]

Source: American Medical Association [12]

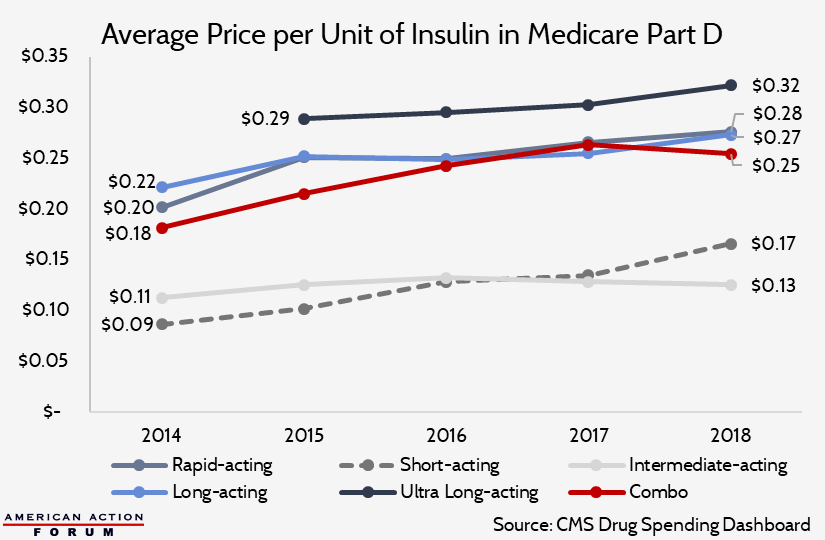

Insulin Spending in Medicare Part D

Medicare spending on insulin has also increased

exponentially over the past decade. Total Part D spending on insulin increased

10-fold from $1.4 billion in 2007 to $14.4 billion in 2018, more than 10 times

faster than enrollment.[13], [14] The top five insulin products in

2018 (in terms of use and total spending) accounted for $8.1 billion (56

percent) of all Part D insulin spending.[15] Spending per person increased 18

percent annually, from nearly $900 in 2007 to roughly $4,000 in 2016, and

beneficiaries’ average out-of-pocket (OOP) costs during this time increased 17

percent annually.[16]

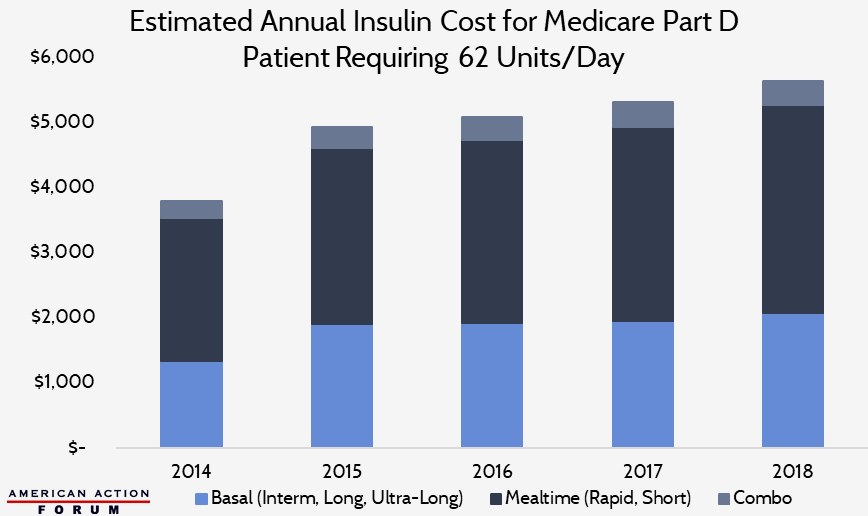

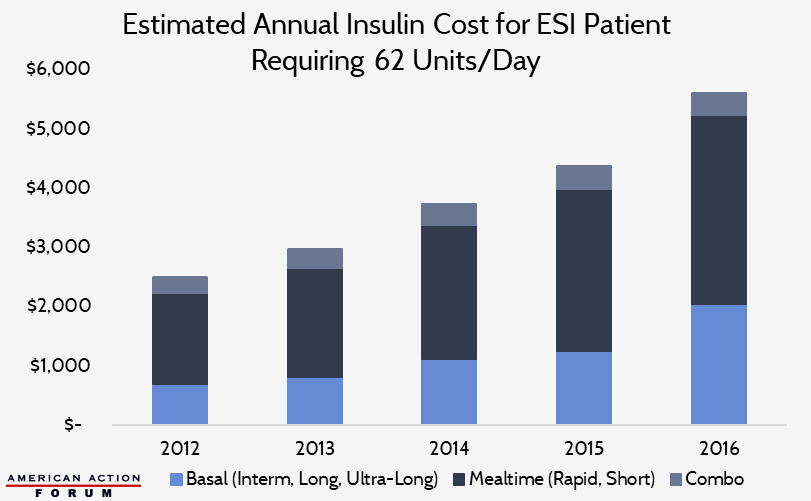

Typical Insulin Spending per Patient

According to the Health Care Cost Institute, the

average insulin user with employer-sponsored insurance (ESI) uses 62 units per

day (approximately 22 basal units, 36 mealtime units, and 4 units of

combination insulin).[17] The following chart shows the

estimated average annual insulin cost for a Medicare Part D patient taking a

similar dosage, based on pricing and spending data from the Centers for

Medicare and Medicaid Services’ Part D Drug Spending Dashboard.[18] Per capita insulin costs in

Medicare Part D, Medicaid, and ESI are all broadly similar and are estimated to

have surpassed $5,600 in 2018, as shown in the Appendix.

The Appendix further details spending and cost

information for Medicaid, Medicare Part D, and patients with ESI.

Estimating Future Costs

With more than 8 million Americans estimated to

be using insulin today at a cost of nearly $6,000 annually per person, insulin

costs (before rebates) account for roughly $48 billion (20 percent) of the

direct medical costs of diabetics.[19] If the share of diabetics requiring

insulin remains steady at 24 percent and 1.5 million Americans continue to be

diagnosed each year, gross insulin costs would increase more than $2 billion

annually if insulin prices and per capita utilization did not change. If

insulin list prices continued to increase at a rate similar to the trend

between 2012 and 2018, gross insulin costs in the United States could reach

$121.2 billion by 2024 (or $12,446 per insulin user), before subtracting

discounts and rebates. If prices continue to increase at the slower rate seen

between 2016 and 2018, gross insulin costs would increase to just $60.7 billion

in 2024 (or $6,263 per patient).

Why Are Prices Increasing?

A number of factors likely contribute to rising

insulin prices, but one of the largest is the existence of large rebates.

Rebates

The current practice of manufacturers offering

large rebates likely contributes to both increasing insulin prices and the limited

uptake of lower-priced products.[20] Pharmacy-benefit

managers (PBMs) are responsible for maintaining insurers’ drug

formularies, or list of prescriptions that are covered by a given insurance

plan, and they generate significant revenue through rebates on brand-name drugs

from manufacturers.[21] PBMs

incentivize drug manufacturers to offer competitively high rebates so their

specific products are included on formularies and given preferential placement.[22] Hence,

competition among drug manufacturers for top-tier allocation of their products

has driven ever-larger rebates, which naturally leads to higher list prices.[23]

While list prices are increasing significantly,

net prices (list prices minus rebates and other discounts) received by

manufacturers have increased much less drastically.[24] For example, Novo Nordisk reported

that between 2001 and 2016, the list price of the NovoLog vial increased 353

percent while the net price increased just 36 percent.[25] The

NovoLog FlexPen list price increased 270 percent between 2003 and 2016, while

its net price only increased 3 percent.[26] Eli

Lilly released similar information showing the list price of Humalog increased

27 percent from 2015 to 2019, while the net price decreased 14 percent.[27] Sanofi’s

latest pricing report shows that since 2012, the average list price for all its

insulin products increased 126 percent by 2018, while the average net price has

decreased 25 percent.[28]

Based on the data provided by these

manufacturers, as well as data from Pharmaceutical Care Management Association

(PCMA), insulin rebates average between 30 and 50 percent, and often reach as

high as 70 percent for the most commonly used insulin products, significantly

higher than the average rebate for other types of drugs.[29] For comparison, the Medicare

Trustees Report shows that rebates for all drugs averaged between 18 and 22

percent in Medicare Part D from 2015 to 2017, while rebates for all products in

Medicaid averaged 51 percent in 2016.[30], [31] Estimates of drug rebates in the

commercial market range from 12 percent to 30 percent in 2018.[32] PCMA maintains that its analysis of

rebates for insulin products indicates there is no correlation between list

price growth and the size of the rebate. It remains true, however, that insulin

rebates are larger, on average, than those provided for other types of drugs,

according to available data.

This discrepancy between list and net price has

a major impact on the amount that insurers and patients ultimately spend on

insulin. According to the American Diabetes Association’s (ADA) 2017 report on

the Economic Costs of Diabetes in the United States, after accounting for

discounts and rebates, insulin costs account for just 6.3 percent of overall

costs, ranging from 4.6 percent of costs for privately insured individuals and

7.2 percent of costs for those enrolled in public programs.[33]

Nevertheless, patients’ insulin costs, on

average, are increasing. Patients’ prescription out-of-pocket (OOP)

costs—increasingly calculated as a percentage of the cost (co-insurance),

rather than a fixed dollar amount (co-payment)—are typically based on a medicine’s

list price, rather than the net price. As list prices rise, so do patients’ OOP

costs. Further, the large rebates do not benefit insulin patients directly.

Insurers and PBMs use rebates primarily to reduce premiums for all enrollees,

rather than reduce patients’ OOP liability. Thus, diabetic patients generally

only benefit indirectly, through low premiums, from the significant rebates and

discounts offered for insulin products.

The rebate structure is also likely at least

partially responsible for the low utilization rates of the less expensive

insulin options currently on the market. Eli Lilly attempted to offer

lower-cost versions of both its pen and injection insulin products (Humalog

Lispro injections in May 2019 and Humalog Kwikpens in January 2020).[34] By

January 2020 (nine months after the release of the half-price Humalog

injections), only 14 percent of U.S. prescriptions for Humalog were for the

half-price version.[35] Pharmacists

and patients claim the half-price Humalog Lispro injections are not readily

available or that they are not covered by the patients’ insurance.[36] Novo

Nordisk announced it

would offer free, one-time insulin supply to patients in immediate need, as

well as expanded affordable options such as a $99 three-pack of vials or a $99

two-pack of their brand-name insulin pens. Last, Sanofi’s Insulin Valyou Savings

Program sets a fixed $99 monthly price on any combination of up

to 10 insulin vials/pens, but the program is only available to uninsured

patients.

If the cheaper products

are purchased (for which rebates are not provided), rather than the more expensive

products for which rebates are offered, insurers and PBMs may experience

reduced revenue. As a result, insurers and PBMs may be unlikely to encourage

patients to use the lower-cost options, perhaps by refusing coverage.

Competition Issues

Ninety-nine percent of

the insulin used in the United States is produced by one of three drug

manufacturers. The lack of robust competition allows insulin prices to remain

high, particularly for the uninsured and those with high cost-sharing insurance

plans. While the regulatory barriers hindering biosimilar insulin supply in the

United States recently expired, as explained here, it is unlikely that

new competition will enter the market overnight.

Regulatory Barriers

Finally, numerous legal

and regulatory changes affecting the broader health care market have likely

also impacted the price of medicines across the board. The Affordable Care Act

(ACA) included several provisions that either reduced drug manufacturer

revenues or increased the cost of selling drugs, primarily by expanding or

creating new programs for which drug manufacturers must provide significant

discounts. A previous American Action Forum study estimated that from

2012-2018, these policy changes cost the pharmaceutical industry roughly $140

billion.[37] Given that, it should not be surprising

that the price of medicines increased during this time.

Results of Increasing

Costs

Rising insulin prices

can cause severe consequences for diabetics. Roughly a quarter of American

diabetics reported rationing their insulin because they cannot afford the cost

of their full prescribed dosage.[38] In 2018, the ADA conducted the Insulin

Affordability Survey, and 39 percent of respondents indicated their insulin

costs had increased from the year prior, while 27 percent said that the increasing

costs of insulin had affected their insulin use or purchase in some way.[39] Of those who were affected, 26 percent

noted regularly taking less than prescribed, 23 percent noted having to change

to less expensive types or brands, and another 23 percent noted missing doses

weekly. Additionally, 36 percent said they were forced to make the choice

between insulin or other health-related services, 32 percent said they had to

make the choice between insulin or transportation, and 30 percent said they had

to make the choice between insulin or paying for their utilities.[40]

Conclusion

Diabetes is now the

costliest chronic condition in the United States, with one fourth of health

care expenditures in the United States spent on patients with diabetes. The

insulin costs for the estimated 8.3 million Americans who require prescription

insulin accounts for roughly 20 percent of the overall cost of treating

diabetes before rebates and discounts are factored in—although after rebates

are accounted for, insulin is responsible for 6.3 percent of overall costs. If

current trends continue, gross annual insulin costs could reach $121.2 billion

by 2024. While regulatory barriers hindering competition in the insulin market

are set to expire soon, changes to current drug pricing practices are likely

also needed to bring costs down.

Appendix

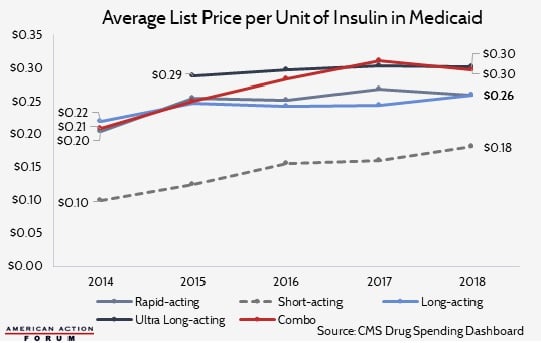

Insulin Costs in

Medicaid

From 1991 to 2014,

Medicaid reimbursements for insulin increased 17.1 percent annually from

roughly $42.8 million to $1.6 billion.[41] Between 2014 and 2018, spending

accelerated, averaging 24.2 percent per year for a cost of $3.9 billion in

2018. Though, as shown by the charts below, this increase was only partially a

result of price increases.[42] Much of the increased spending during this

period is due to rapid increases in Medicaid enrollment as a result of the

ACA Medicaid expansion.

The estimated average

cost per Medicaid patient using a standard dosage of insulin (22 units of basal

insulin, 36 units of mealtime insulin, and 4 units of combination insulin) is

depicted in the next chart, reaching $5,800 in 2018.[43]

Insulin Costs in the

Employer Market

According to the Health

Care Cost Institute, annual per capita insulin costs for diabetics with ESI

averaged $2,864 in 2012; by 2016, average costs had climbed to $5,705.[44] The chart below shows estimated annual

costs for an insulin patient in the ESI market, taking a standard dose of 62

units per day.[45]

Insulin Spending in

Medicare Part D

Total Part D spending on

insulin increased 10-fold from $1.4 billion in 2007 to $14.4 billion in 2018,

more than 10 times faster than enrollment.[46], [47] Another $367 million was spent on insulin

administration supplies (syringes, needles, pens, pumps, etc.) in 2018.[48] Spending per person increased 18 percent

annually from nearly $900 in 2007 to roughly $4,000 in 2016, and beneficiaries’

average OOP costs during this time increased 17 percent annually.[49] The average price per dosage unit

increased 10.1 percent per year from 2014 to 2018.[50]

Based on these data from

the Centers for Medicare and Medicaid Services’ Part D Drug Spending Dashboard,

the following chart shows the estimated average annual insulin cost for a

Medicare Part D patient requiring 62 units per day (22 basal units, 36 mealtime

units, and 4 units of combination insulin). Per capita insulin costs in Part D

surpassed $5,600 in 2018.

[1] https://connect.asmbs.org/07-2018/american-diabetes-association-report-diabetes-is-the-most-expensive-chronic-disease-in-america

[5] https://healthcostinstitute.org/diabetes-and-insulin/spending-on-individuals-with-type-1-diabetes-and-the-role-of-rapidly-increasing-insulin-prices

[7] https://care.diabetesjournals.org/content/diacare/suppl/2018/03/20/dci18-0007.DC1/DCi180007SupplementaryData.pdf

[8] http://www.natap.org/2019/HIV/ioi150073.pdf, https://www.uofmhealth.org/news/archive/201604/sugar-shock-insulin-costs-tripled-10-years-study-finds, https://healthcostinstitute.org/diabetes-and-insulin/price-of-insulin-prescription-doubled-between-2012-and-2016, https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/Information-on-Prescription-Drugs

[9] https://healthcostinstitute.org/diabetes-and-insulin/spending-on-individuals-with-type-1-diabetes-and-the-role-of-rapidly-increasing-insulin-prices

[11] Authors’

calculation based on CMS Medicaid Drug Spending Dashboard data: https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/Information-on-Prescription-Drugs/Medicaid

[14] 2018

estimates are authors’ calculations based on data obtained from CMS’s Medicare

Part D Drug Spending Dashboard: https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/Information-on-Prescription-Drugs/MedicarePartD

[15] Products

include: Lantus Solostar, Levemir Flextouch, Lantus, Novolog Flexpen, and

Humalog Kwikpen U-100. Authors’ calculations based on data obtained from CMS’s

Medicare Part D Drug Spending Dashboard: https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/Information-on-Prescription-Drugs/MedicarePartD

[17] https://healthcostinstitute.org/diabetes-and-insulin/spending-on-individuals-with-type-1-diabetes-and-the-role-of-rapidly-increasing-insulin-prices

[18] https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/Information-on-Prescription-Drugs/MedicarePartD

[19] This

estimate does not account for the value of rebates provided for insulin as that

information is not publicly available and thus was not included in the study conducted

by the Health Care Cost Institute or the data available on the CMS Drug

Spending Dashboards which are the basis for this estimate.

[27]https://assets.ctfassets.net/srys4ukjcerm/4eLJOMYz0ZOsvxx8QqmxEb/111ae072aba877601c2e0cc836ded5dc/Lilly-2019-Integrated-Summary-Report.pdf

[28] https://www.sanofi.us/-/media/Project/One-Sanofi-Web/Websites/North-America/Sanofi-US/Home/corporateresponsibility/Prescription_Medicine_Pricing_2019.pdf?sf208075846=1

[30] https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/ReportsTrustFunds/Downloads/TR2019.pdf

[33] https://care.diabetesjournals.org/content/diacare/suppl/2018/03/20/dci18-0007.DC1/DCi180007SupplementaryData.pdf

[34]https://www.reuters.com/article/us-lilly-insulin/eli-lilly-to-launch-half-priced-versions-of-two-more-insulin-products-idUSKBN1ZD1JN

[35]https://assets.ctfassets.net/srys4ukjcerm/4eLJOMYz0ZOsvxx8QqmxEb/111ae072aba877601c2e0cc836ded5dc/Lilly-2019-Integrated-Summary-Report.pdf

[36]https://www.politico.com/newsletters/prescription-pulse/2019/10/11/access-issues-drug-shortages-dictate-pharmacy-fills-in-q3-780208

[37] https://www.americanactionforum.org/insight/understanding-the-policies-that-influence-the-cost-of-drugs/

[42] https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/Information-on-Prescription-Drugs/Medicaid

[43] Utilization

rates have been increased from 40 units per day (used in the AMA study) to 60

units per day to better match today’s average utilization, as found in the HCCI

report: https://healthcostinstitute.org/diabetes-and-insulin/spending-on-individuals-with-type-1-diabetes-and-the-role-of-rapidly-increasing-insulin-prices

[44] https://healthcostinstitute.org/diabetes-and-insulin/spending-on-individuals-with-type-1-diabetes-and-the-role-of-rapidly-increasing-insulin-prices

[45] https://healthcostinstitute.org/diabetes-and-insulin/price-of-insulin-prescription-doubled-between-2012-and-2016

[47] 2018

estimates are authors’ calculations based on data obtained from CMS’s Medicare

Part D Drug Spending Dashboard: https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/Information-on-Prescription-Drugs/MedicarePartD

[48] Authors’

calculations based on data obtained from CMS’s Medicare Part D Drug Spending

Dashboard: https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/Information-on-Prescription-Drugs/MedicarePartD

[50] Authors’

calculations based on data obtained from CMS’s Medicare Part D Drug Spending

Dashboard: https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/Information-on-Prescription-Drugs/MedicarePartD

https://www.americanactionforum.org/research/insulin-cost-and-pricing-trends/#ixzz6IYNwWIrA

Follow @AAF on Twitter

This comment has been removed by a blog administrator.

ReplyDelete