Andrew Strohman, Health Care Data Analyst

The RAND Corporation recently published a report

assessing the potential impact of a Medicare buy-in. While its results on

enrollment are similar to those reported in AAF’s

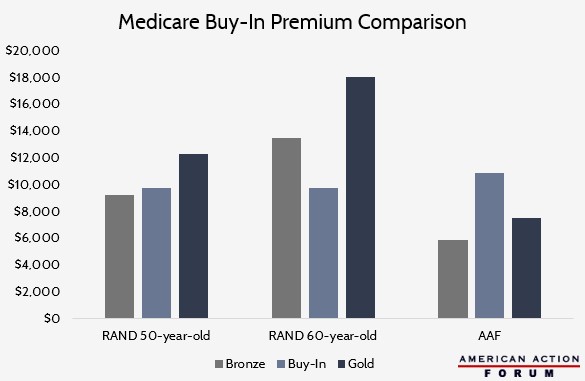

model of H.R. 1346, which would also allow those aged 50-64 to enroll in

Medicare, there are some differences in its projected premiums. AAF’s projected

2022 average buy-in premium is $10,900, significantly higher than the $9,747

premium projected for both 50- and 60-year-old buy-in enrollees under RAND’s

projection for the same year. Additionally, AAF projects the buy-in premium

will be higher than both the average Bronze and Gold plans, while RAND expects

buy-in premiums to be lower than at least the Gold plan.

These disparities may come from subtle

differences in assumptions for the modeling. While both assumed actuarial

values (AV) of 80 percent (equivalent to a Gold plan) and roughly the same

national average ratio of payment rates (between 84-86 percent), RAND assumed

that those who qualified for cost-sharing reduction (CSR) payments would

receive plans with AVs of 94, 87, and 73 percent as household income approached

250 percent of the federal poverty level (FPL). AAF specifically modelled H.R.

1346, using its proposed expanded CSR eligibility with AVs of 95, 90, and

85 percent up to 400 percent of the FPL. Furthermore, AAF assumed the

reintroduction of an individual mandate penalty while RAND kept it zeroed out.

Finally, RAND seems to model the average premiums offered while AAF

models premiums paid. These alternative assumptions may explain the

different final premiums.

https://www.americanactionforum.org/weekly-checkup/a-surprisingly-busy-week-in-health-policy/#ixzz69cXjHe1f

Follow @AAF on Twitter

Follow @AAF on Twitter

No comments:

Post a Comment